Appendix Ex 25-26 Variable cost concept of product pricing

Based on the data presented in Exercise 25-17, assume that Smart Stream Inc. uses the variable cost concept of applying the cost-plus approach to product pricing.

a. Determine the variable costs and the variable cost amount per unit for the production and sale of 10,000 cellular phones.

b. Determine the variable cost markup percentage (rounded to two decimal places) for cellular phones.

c. Determine the selling price of cellular phones. Round to the nearest dollar.

Answer:

{kind=link}

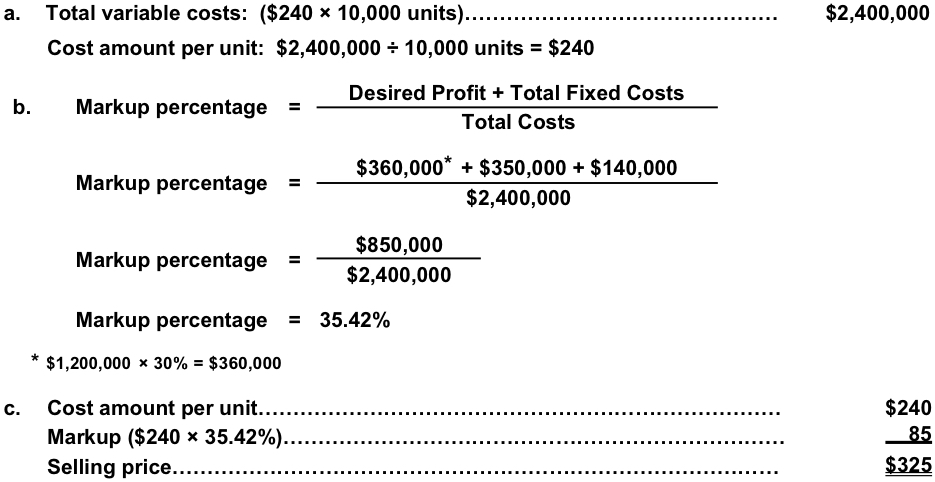

a. Total variable costs: ($240 × 10,000 units)……………………………………… $2,400,000

Cost amount per unit: $2,400,000 ÷ 10,000 units = $240

b. Markup percentage =

Markup percentage =

Markup percentage =

Desired Profit + Total Fixed Costs

Total Costs

EX 26-2 Average rate of return—cost savings

Midwest Fabricators Inc. is considering an investment in equipment that will replace direct labor. The equipment has a cost of $132,000 with a $16,000 residual value and a 10-year

life. The equipment will replace one employee who has an average wage of $34,000 per year. In addition, the equipment will have operating and energy costs of $5,380 per year.

Determine the average rate of return on the equipment, giving effect to straight-line depreciation on the investment.

Answer:

{kind=link}

Average Rate

of Return =

=

Average Annual Income

Average Investment

Average Savings* – Annual Depreciation – Additional Operating Costs

(Beginning Cost + Residual Value) ÷ 2

$34,000 – [($132,000 – $16,000) ÷ 10 years] – $5,380

=

($132,000 + $16,000) ÷ 2

= $17,020

$74,000

= 23%

* The effect of the savings in wages expense is an increase in income.

Accounting Q and A

EX 26-2 Average rate of return—cost savings

Midwest Fabricators Inc. is considering an investment in equipment that will replace direct labor. The equipment has a cost of $132,000 with a $16,000 residual value and a 10-year

life. The equipment will replace one employee who has an average wage of $34,000 per year. In addition, the equipment will have operating and energy costs of $5,380 per year.

Determine the average rate of return on the equipment, giving effect to straight-line depreciation on the investment.

Answer:

Average Rate

of Return =

=

Average Annual Income

Average Investment

Average Savings* – Annual Depreciation – Additional Operating Costs

(Beginning Cost + Residual Value) ÷ 2

$34,000 – [($132,000 – $16,000) ÷ 10 years] – $5,380

=

($132,000 + $16,000) ÷ 2

= $17,020

$74,000

= 23%

* The effect of the savings in wages expense is an increase in income.

EX 26-1 Average rate of return

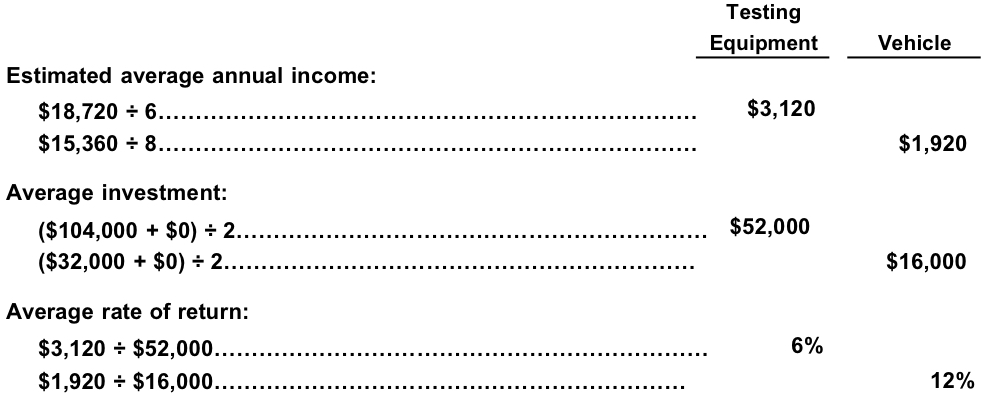

The following data are accumulated by Bio Metrics Inc. in evaluating two competing capital investment proposals:

Testing Equipment | Vehicle

Amount of investment $104,000 | $32,000

Useful life 6 years | 8 years

Estimated residual value 0 | 0

Estimated total income over the

useful life $18,720 | $15,360

Determine the expected average rate of return for each proposal.

Answer:

Testing

Equipment Vehicle

$18,720 ÷ 6……………………………………………………………… $3,120

$15,360 ÷ 8……………………………………………………………… $1,920

Average investment:

($104,000 + $0) ÷ 2……………………………………………………… $52,000

($32,000 + $0) ÷ 2……………………………………………………… $16,000

Average rate of return:

$3,120 ÷ $52,000………………………………………………………… 6%

$1,920 ÷ $16,000……………………………………………………… 12%

{kind=link}

Appendix Ex 25-26 Variable cost concept of product pricing

Based on the data presented in Exercise 25-17, assume that Smart Stream Inc. uses the variable cost concept of applying the cost-plus approach to product pricing.

a. Determine the variable costs and the variable cost amount per unit for the production and sale of 10,000 cellular phones.

b. Determine the variable cost markup percentage (rounded to two decimal places) for cellular phones.

c. Determine the selling price of cellular phones. Round to the nearest dollar.

Answer:

a. Total variable costs: ($240 × 10,000 units)……………………………………… $2,400,000

Cost amount per unit: $2,400,000 ÷ 10,000 units = $240

b. Markup percentage =

Markup percentage =

Markup percentage =

Desired Profit + Total Fixed Costs

Total Costs

$360,000* + $350,000 + $140,000

$2,400,000

$850,000

$2,400,000

Markup percentage = 35.42%

* $1,200,000 × 30% = $360,000

c. Cost amount per unit………………………………………………………………… $240

Markup ($240 × 35.42%)……………………………………………………………… 85

Selling price…………………………………………………………………………… $325

Appendix Ex 25-25 Total cost concept of product pricing

Based on the data presented in Exercise 25-17, assume that Smart Stream Inc. uses the total cost concept of applying the cost-plus approach to product pricing.

a. Determine the total costs and the total cost amount per unit for the production and sale of 10,000 cellular phones.

b. Determine the total cost markup percentage (rounded to two decimal places) for cellular phones.

c. Determine the selling price of cellular phones. Round to the nearest dollar.

Answer:

{kind=link}

a. Total costs:

Variable ($240 × 10,000 units)………………………………………………… $2,400,000

Fixed ($350,000 + $140,000)……………………………………………………… 490,000

Total……………………………………………………………………………………… $2,890,000

Cost amount per unit: $2,890,000 ÷ 10,000 units = $289

b. Markup percentage =

Markup percentage =

Desired Profit

Total Costs

$360,000*

$2,890,000

Markup percentage = 12.46% (rounded)

* $1,200,000 × 30% = $360,000

c. Cost amount per unit………………………………………………………………… $289

Markup ($289 × 12.46%)……………………………………………………………… 36

Selling price…………………………………………………………………………… $325

Ex 25-24 Activity rates and product costs using activity-based costing

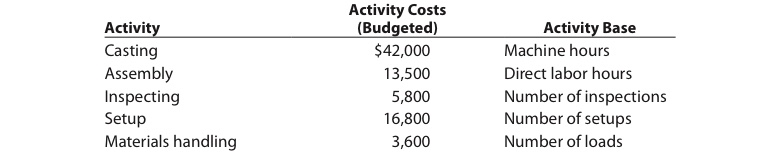

BriteLite Inc. manufactures entry and dining room lighting fixtures. Five activities are used in manufacturing the fixtures. These activities and their associated activity costs and activity bases are as follows:

{kind=link}

Activity

Activity Costs

(Budgeted)

Activity Base

Casting $42,000 Machine hours

Assembly 13,500 Direct labor hours

Inspecting 5,800 Number of inspections

Setup 16,800 Number of setups

Materials handling 3,600 Number of loads

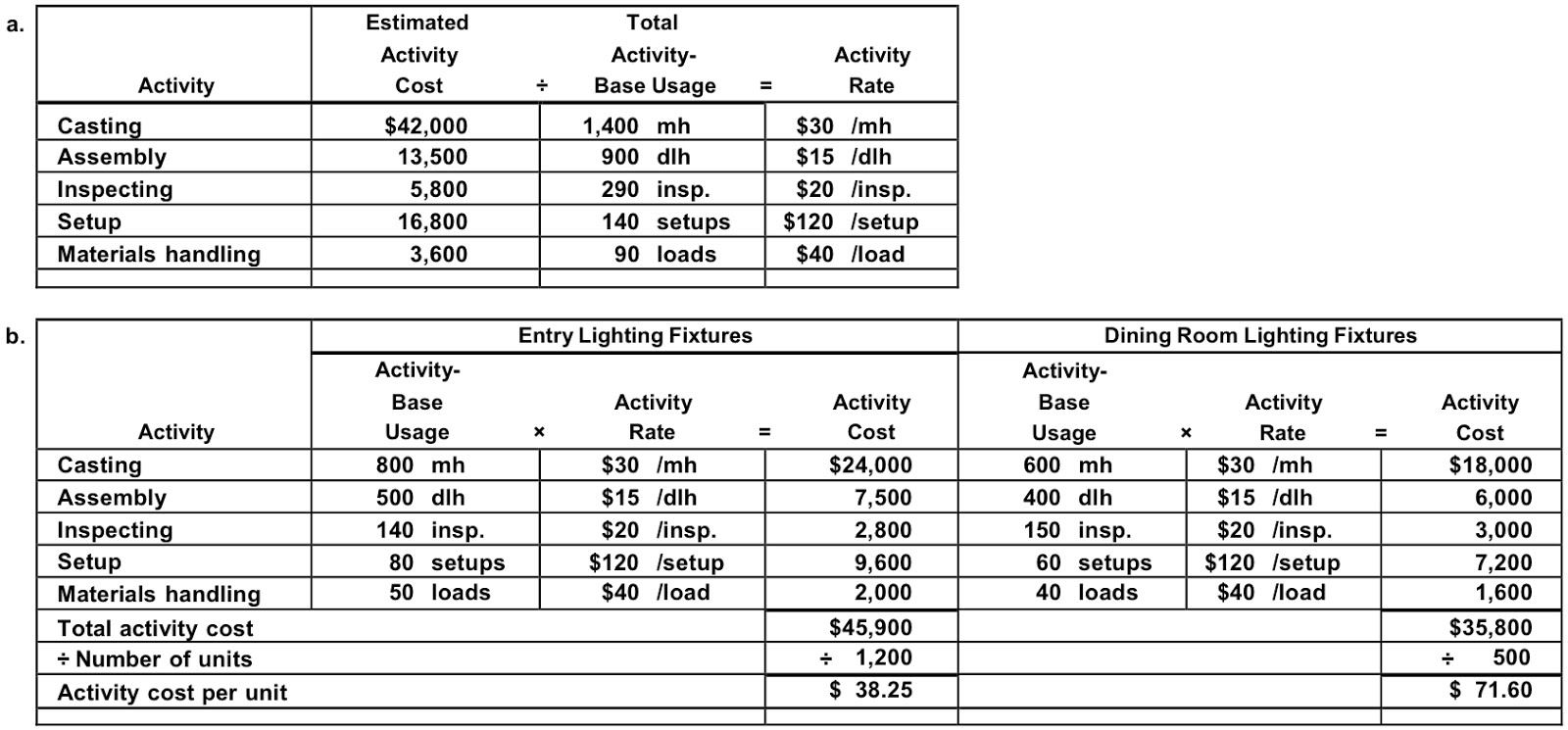

Corporate records were obtained to estimate the amount of activity to be used by the two products. The estimated activity-base usage quantities and units produced for each product and in total are provided in the table below.

Activity Base | Entry | Dining | Total

Machine hours | 800 | 600 | 1,400

Direct labor hours | 500 | 400 | 900

Number of inspections. | 140 | 150 | 290

Number of setups | 80 | 60 | 140

Number of loads | 50 | 40 | 90

Units produced | 1,200 | 500 | 1,700

a. Determine the activity rate for each activity.

b. Use the activity rates in (a) to determine the total and per unit activity costs associated with each product.

Answer:

{kind=link}

Estimated Total

Activity Activity- Activity

Cost ÷ Base Usage = Rate

Casting $42,000 1,400 mh $30 /mh

Assembly 13,500 900 dlh $15 /dlh

Inspecting 5,800 290 insp. $20 /insp.

Setup 16,800 140 setups $120 /setup

Materials handling 3,600 90 loads $40 /load

Activity

Entry Lighting Fixtures Dining Room Lighting Fixtures

Activity-

Base Activity Activity

Usage × Rate = Cost

Casting 800 mh $30 /mh $24,000 600 mh $30 /mh $18,000

Assembly 500 dlh $15 /dlh 7,500 400 dlh $15 /dlh 6,000

Inspecting 140 insp. $20 /insp. 2,800 150 insp. $20 /insp. 3,000

Setup 80 setups $120 /setup 9,600 60 setups $120 /setup 7,200

Materials handling 50 loads $40 /load 2,000 40 loads $40 /load 1,600

Total activity cost $45,900 $35,800

÷ Number of units ÷ 1,200 ÷ 500

Activity cost per unit $ 38.25 $ 71.60

Ex 25-23 Activity-based costing

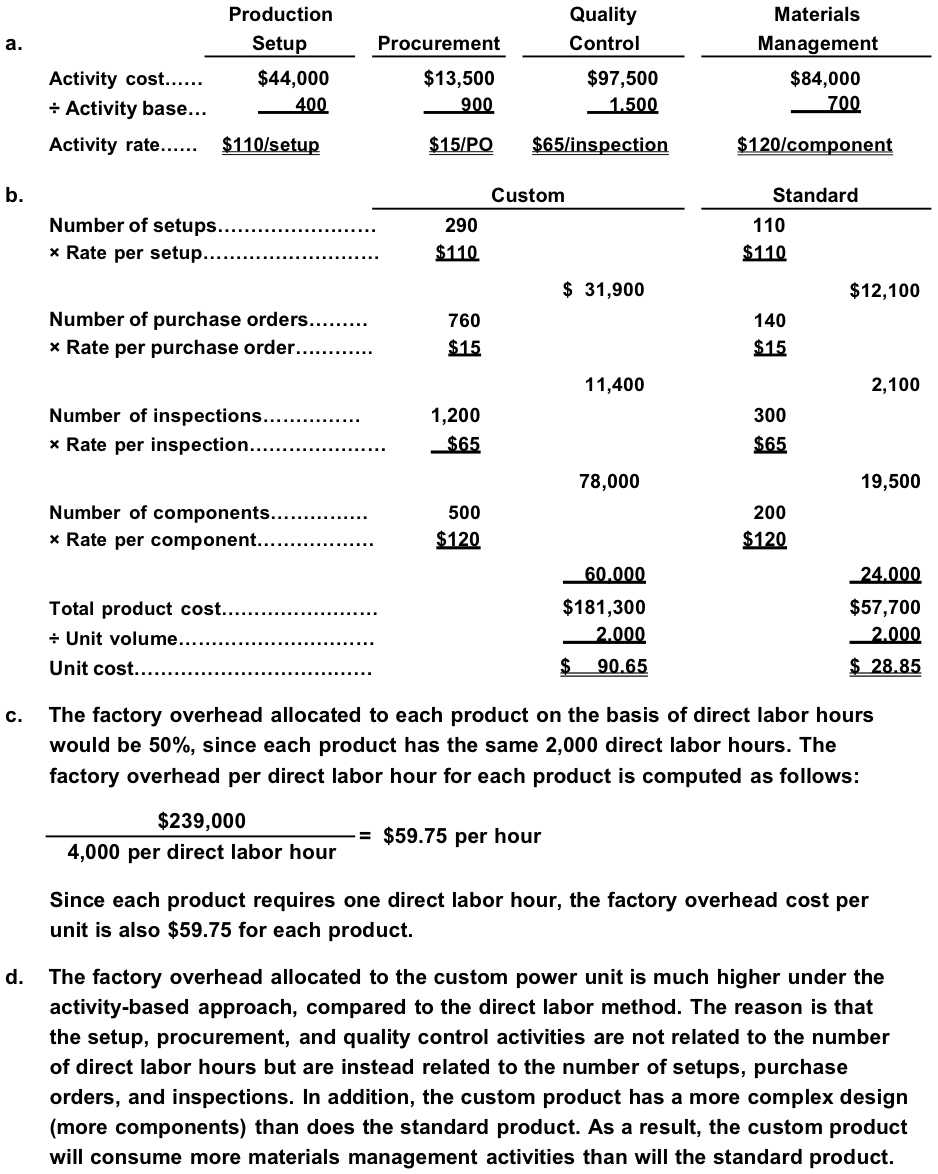

Zeus Industries manufactures two types of electrical power units, custom and standard, which involve four factory overhead activities—production setup, procurement, quality control, and materials management. An activity analysis of the overhead revealed the following estimated activity costs and activity bases for these activities:

{kind=link}

Activity Activity Cost Activity Base

Production setup $ 44,000 Number of setups

Procurement 13,500 Number of purchase orders (PO)

Quality control 97,500 Number of inspections

Materials management 84,000 Number of components

Total$239,000p

The activity-base usage quantities for each product are as follows:

Setups

Purchase

Orders Inspections Components Unit Volume

Custom 290 760 1,200 500 2,000

Standard 110 140 300 200 2,000

Total 400 900 1,500 700 4,000

a. Determine an activity rate for each activity.

b. Assign activity costs to each product, and determine the unit activity cost, using the activity rates from part (a).

c. Assume that each product required one direct labor hour per unit. Determine the per unit cost if factory overhead is allocated on the basis of direct labor hours.

d. Explain why the answers in parts (b) and (c) are different.

Answer:

{kind=link}

Production Quality

Materials

a. Setup Procurement Control

Activity cost…… $44,000 $13,500 $97,500

÷ Activity base… 400 900 1,500

Activity rate…… $110/setup $15/PO $65/inspection

Management

$84,000

700

$120/component

b. Custom Standard

Number of setups…………………… 290 110

× Rate per setup……………………… $110 $110

Number of purchase orders………

760

$ 31,900

140

$12,100

× Rate per purchase order………… $15 $15

11,400 2,100

Number of inspections…………… 1,200 300

× Rate per inspection………………… $65 $65

78,000 19,500

Number of components…………… 500 200

× Rate per component……………… $120 $120

60,000 24,000

Total product cost…………………… $181,300 $57,700

÷ Unit volume………………………… 2,000 2,000

Unit cost……………………………… $ 90.65 $ 28.85

c. The factory overhead allocated to each product on the basis of direct labor hours

would be 50%, since each product has the same 2,000 direct labor hours. The

factory overhead per direct labor hour for each product is computed as follows:

$239,000

4,000 per direct labor hour

= $59.75 per hour

Since each product requires one direct labor hour, the factory overhead cost per

unit is also $59.75 for each product.

d. The factory overhead allocated to the custom power unit is much higher under the

activity-based approach, compared to the direct labor method. The reason is that

the setup, procurement, and quality control activities are not related to the number

of direct labor hours but are instead related to the number of setups, purchase

orders, and inspections. In addition, the custom product has a more complex design

(more components) than does the standard product. As a result, the custom product

will consume more materials management activities than will the standard product.

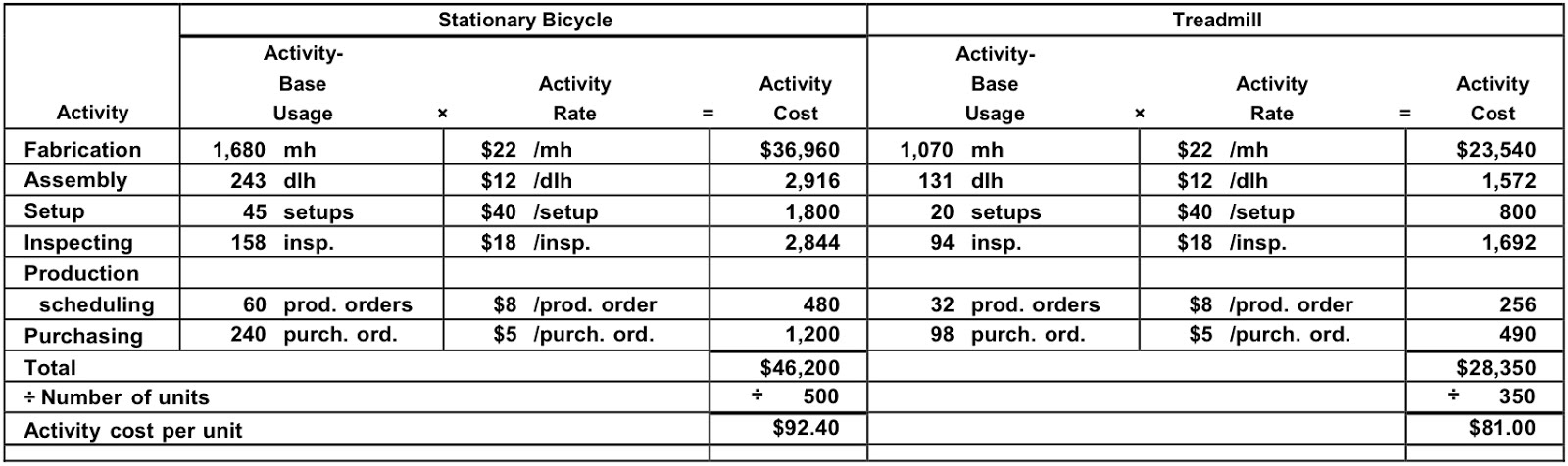

Ex 25-22 Activity-based costing

CardioTrainer Equipment Company manufactures stationary bicycles and treadmills. The products are produced in the Fabrication and Assembly production departments. In addition to production activities, several other activities are required to produce the two products. These activities and their associated activity rates are as follows:

Activity | Activity Rate

Fabrication | $22 per machine hour (mh)

Assembly | $12 per direct labor hour (dlh)

Setup | $40 per setup

Inspecting | $18 per inspection

Production scheduling | $8 per production order

Purchasing | $5 per purchase order

The activity-base usage quantities and units produced for each product were as follows:

Stationary Bicycle | Treadmill

Machine hours 1,680 | 1,070

Direct labor hours 243 | 131

Setups 45 | 20

Inspections 158 | 94

Production orders 60 | 32

Purchase orders 240 | 98

Units produced 500 | 350

Use the activity rate and usage information to compute the total activity costs and the activity costs per unit for each product.

Answer:

Stationary Bicycle Treadmill

Activity-

Base Activity Activity

Usage × Rate = Cost

Activity-

Base Activity Activity

Usage × Rate = Cost

Fabrication 1,680 mh $22 /mh $36,960 1,070 mh $22 /mh $23,540

Assembly 243 dlh $12 /dlh 2,916 131 dlh $12 /dlh 1,572

Setup 45 setups $40 /setup 1,800 20 setups $40 /setup 800

Inspecting 158 insp. $18 /insp. 2,844 94 insp. $18 /insp. 1,692

Production

scheduling 60 prod. orders $8 /prod. order 480 32 prod. orders $8 /prod. order 256

Purchasing 240 purch. ord. $5 /purch. ord. 1,200 98 purch. ord. $5 /purch. ord. 490

Total $46,200 $28,350

÷ Number of units ÷ 500 ÷ 350

Activity cost per unit $92.40 $81.00

{kind=link}